Engagement Problems at Nextdoor

Engagement Problems at Nextdoor

How poor user demographics and a misguided use case are hurting the company

New analysis is posted every Monday at 10 am ET. Subscribe to Theta Thoughts to get posts that give you a premium for your time directly in your inbox!

Disclaimer: I hold no position in Nextdoor. This and all posts on Theta Thoughts are my thoughts alone and should not be constituted as investment advice.

Acronyms: DAU = Daily Active User | WAU = Weekly Active Active User | ARPU = Average Revenue Per User

Nextdoor (NYSE: KIND - $2.638 billion) is a hyperlocal social networking app that enables its users to connect with people in their neighborhood. Despite running into a massive cash pile in its SPAC merger last year, the company is facing systemic engagement and demographic issues that are blunting its growth prospects. Even if revenue increases by over 35% next year, the stock has the potential to lose over a third of its value in my opinion.

Demographic Problems

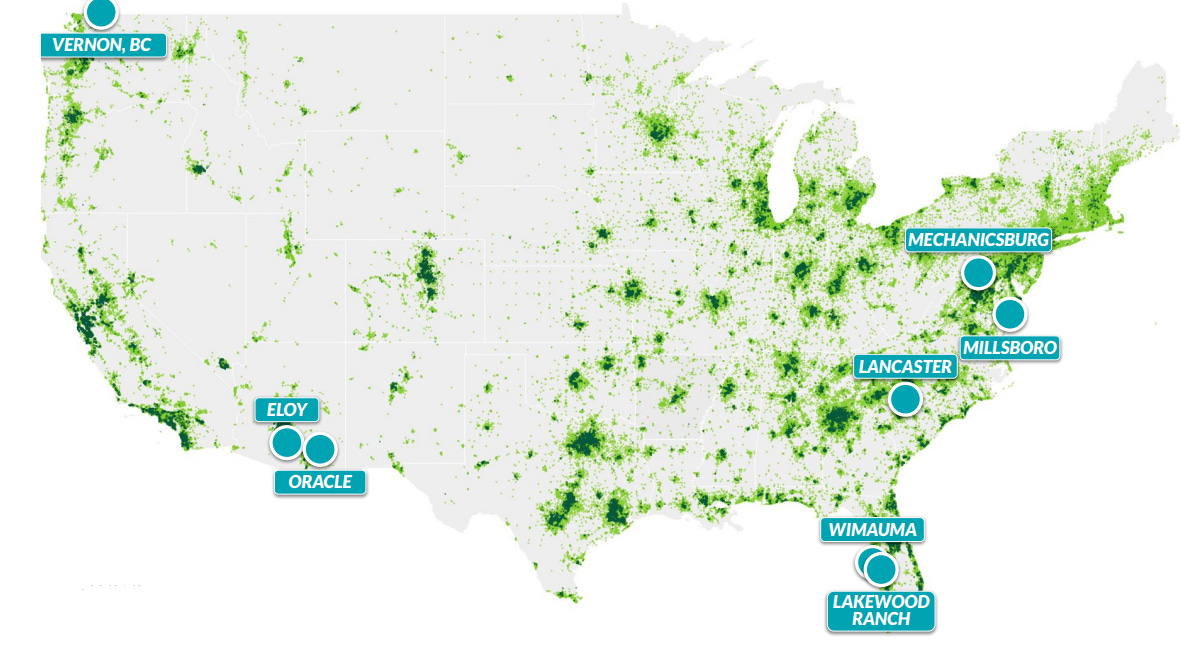

Nextdoor has been around since 2011, garnering around 66 million registered users in the past 11 years since its founding. However, the company’s value proposition has caused the app to reach high local engagement primarily among older users in suburban or rural locations, not in cities.

Out of their top engagement locations listed in the United States: Eloy and Oracle in Arizona, Wimauma and Lakewood Ranch in Florida, Lancaster in South Carolina, Millsboro in Delaware, and Mechanicsburg in Pennsylvania, only one has a population of over 12,500, and the median age in all but Wimauma and Eloy are greater than the national median.

I’ll address the age topic first. Nextdoor doesn’t release age demographic data directly in any disclosures. Usually, a lack of info is to protect against competition or to prevent having to be expected to update a metric over time in the case it worsens. Based on some of the data Nextdoor has disclosed, I’m willing to bet it’s the latter.

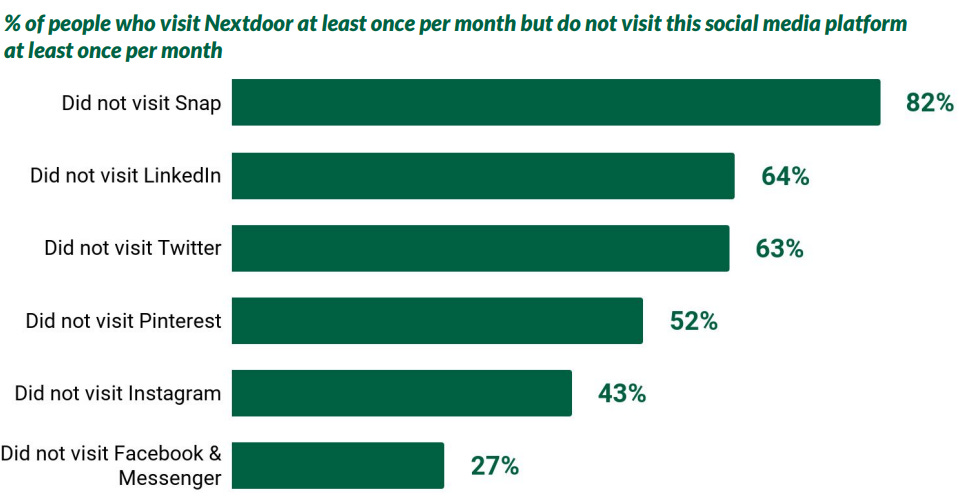

While unintentional, this data that Nextdoor presented as showing how “brands can reach an incremental audience”, shows that they do not have young users on their app whatsoever. According to a study by AudienceProject in late 2020, 48% of internet users in the United States were actively using Snapchat, a number that has only grown in the past year. By publishing data saying that 82% of Nextdoor MAUs are also not Snapchat MAUs, it can be deduced that young users are not being onboarded to the app. What’s more, the app most correlated with active usage of Nextdoor is Facebook, the app that just 27% of teenagers now use.

To me, the inability to onboard younger users is a major issue because those are the people that statistically will be more engaged on social platforms and drive long-term ARPU growth potential. When combined with the geographic distribution of high-engagement neighborhoods it leads me to the conclusion that the company’s current saturation level is materially lower than the TAM they represent in their presentations.

From the cities with the best engagement in the United States that I mentioned earlier, the fact that none had populations over 25,000 and that 4/6 had populations under 10,000 stuck out to me as a concerning sign just as much as the age skew of users. If the company is only getting its best engagement in places without dense populations, then the company is blunting its growth by sealing off its potential in smaller population centers. I believe this is somewhat correlated with the age issue, cities have a younger median age than the nationwide average, which as mentioned is lower than the expected median of users on the app. However, I also think that the company’s value proposition is directly diluted by cities.

Nextdoor pitches itself as a way to stay connected with your neighborhood, but where is that needed more? In a city where tens of thousands of people are on top of each other, or in a more rural place where you can’t see people in your community as easily? The answer in my mind is simply the latter. The result of this is a company that pitches itself being in just 45 million of a reachable 312 million households when I believe the reality is that their potential is much smaller.

Engagement & Use Case Problems

From a mix of the demographic issues already written about and a use case not geared towards high levels of usage, Nextdoor is facing significant engagement issues. The latter is particularly important since their use case being “utility” rather than engagement and time on-app can be counterintuitive to long-term success. Take this quote from their most recent conference call

because actually what you want is the person to come and get something done. They want to do it as fast as possible. So, areas like Search, Discovery, Ask a Neighbor or Find Service, which is on marketplace, we want people to get that done quickly. And so, in fact, time spent on app might actually be the antithesis of what you're trying to get done. So, that's why we look beyond time on the site and use different metrics to say, internally, are these being successful products. (Third quarter conference call)

For a social network to say that time on an app could be the antithesis of what users of their platform are trying to do is something that concerns me greatly. If their primary source of revenue generation is selling ads to users based on the data they collect, this use case directly impairs the company’s objectives. It’s not like Yelp where user-generated reviews make the utility more valuable, it’s a social network that needs engagement to grow in value.

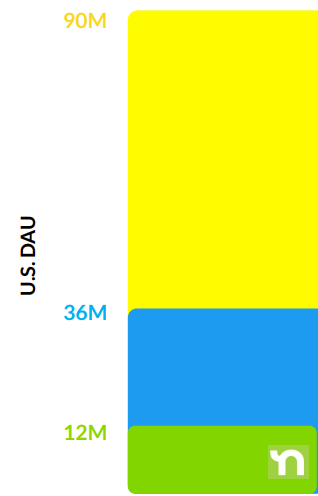

This concern manifests itself in the company’s engagement data. Out of over 66 million verified accounts, only about 31 million are WAUs, with an under 50% conversion rate. More worrying is that out of over 53 million verified users in the United States, just 12 million are DAUs. That’s a conversion rate of just 22.6%.

Assuming that WAUs are evenly distributed based on the geography of verified accounts, that means that only 46% of the over 26 million WAUs in the United States are DAUs. Knowing that Facebook’s apps, which are also facing flagging engagement, have over 65% of their MAUs being DAUs despite that being a much harder hurdle creates substantial concern about the ability to generate growth in monetization if the engagement just isn’t there for it.

There’s also a substantial issue with their paid user acquisition, which makes up 32% of US and a much larger amount of international user acquisition. The company states in public releases that the average payback period on paid user acquisition is five quarters. However, they also state that of new users, only 59% are still active after one year. This means that over 41% of paid acquired users generate losses for the company as they disconnect before Nextdoor gets their money back. The struggle to generate sustained engagement from users the company pays to obtain is concerning to me.

The Valuation

The problems I mentioned are certainly material, but they don’t matter much if the valuation is in-line. The stock has been highly volatile since its de-SPAC, but ambiguity should be embraced when it comes to stocks so let’s go.

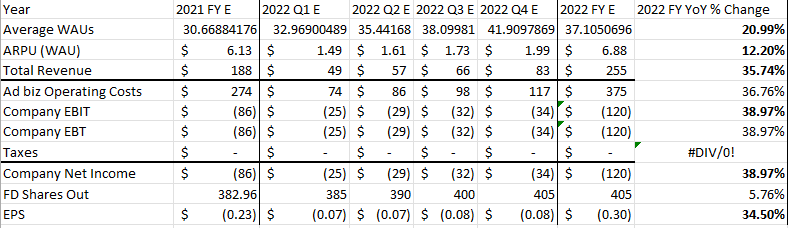

Like Facebook, I made a model that calculates revenue based on active users and ARPU. For Nextdoor this was based on WAUs since it’s their preferred method in their public releases

While there is limited coverage from sell-side analysts, only Evercore and Goldman cover the company to my knowledge, I don’t necessarily disagree with them on a revenue runway. What I likely diverge from them is my expectations on the cost structure of that growth. While the sell-side expects margins to materially improve and for Nextdoor’s net loss to shrink this year, I believe that their poor engagement and demographic metrics mean they will spend their SPAC money more aggressively to acquire users, leading to stronger user growth and worse ARPU gains.

My belief in decelerating ARPU growth is partially rooted in the steep deceleration that will likely be observed in Q4’s results. While 2020 saw Q4 ARPU grow by over 59%, it looks like this will drop to just 17.57% in 2021 for the same quarter. I think the fact that their platform can increase its monetization gives some protection and I do see some reacceleration in ARPU growth in the back half of the year, though this remains under 15%.

I also call for some dilution due to SPAC agreements and the likelihood of continued share-based compensation to employees. Since the company will likely be generating losses for the next several years, I can’t use P/E or EV/EBITDA to attempt valuing it. Instead, I’m using EV/Sales in this scenario.

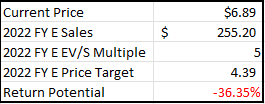

My model bases its price target on my 2022 sales forecast, an EV/Sales multiple of 5x, and assumes a net cash balance of $500 million at the end of 2022 after accounting for my base case’s burn rate. With these considerations, my price target for the stock is $4.39, representing a downside of over 36% from its February 11th closing price of $6.89. While I think Nextdoor can continue to gain users and grow its ARPU, I believe its systemic demographic and engagement issues make the stock worth significantly less than where it is currently valued.

This article is not investment advice and only represents the thoughts of Strat Becker. You can reach me by email at RealStratBeckerYT@gmail.com, on Twitter @StratBecker, or on Commonstock @Strat. This article is for subscribers of the Theta Thoughts newsletter. If this was shared with you please consider subscribing to receive free stock analysis like this every Monday.