Fighting Cyclical Headwinds With Secular Tailwinds

How Winnebago is trying to fight a turning tide

New analysis is posted every Monday at 10 am ET. Subscribe to Theta Thoughts to get posts that give you a premium for your time directly in your inbox!

This newsletter is a project to further grow my research and writing skills. If you have any constructive feedback please leave a comment or send an email! I’d love to hear what you have to say.

I will be discussing the Facebook bear thesis I posted in early January and their earnings in-depth on my Twitch stream tonight. Feel free to stop by from 6:30-8:30pm Eastern Time!

If there’s one thing the pandemic taught us all, it’s that people hate to stay inside. While memes are abundant online about how people need to “touch grass”, everyone has to leave the custom-built caves that we call homes every now and then.

When the pandemic started almost two years ago, there were adjustments I made to my life to prevent myself from feeling cooped up. I went outside more often, even if this was just in the backyard. Neighborhood walks were also incorporated into my routine, a first considering the area I live in doesn’t have any sidewalks.

This cabin fever swept across America, with outdoor lifestyle activities seeing a surge in popularity. I doubt this could be captured better than the surge in RV demand did. Using tools like Google Trends, the mass of people flocking to outdoor trends is clearly visible.

While this surge in demand and the pricing power that followed due to supply shortages was a major boon to RV companies, it has become increasingly clear that cyclical headwinds are rearing their ugly head once again for the industry. With producers running the risk of overshooting a supply equilibrium as has been the case historically, unique strategies are being employed by companies to mitigate the upcoming pressures.

Headwinds are Here

The RV space is one that tends to be cyclical, and I don’t just mean your annual seasonality. Supply/demand equilibrium is a finicky thing in this space, with demand surges and subsequent supply overshoots being commonplace in its history. The pandemic brought unique tailwinds to the space through the change in peoples’ lifestyles that I talked about, but headwinds are quickly emerging.

To start, nationwide dealer channel checks from an analyst team covering Winnebago indicate that supply is beginning to build. Despite the desire for more inventory and to somewhat limit inventory turns, the big news is that supply normalization, especially in the towables segment is expected to occur far faster than before.

The problem is that this normalization isn’t happening just because of supply chains sorting themselves out. They remain an issue, especially with semiconductors if the renewed drop in auto production indicates anything. However, there are also headwinds that are reducing a potential customer’s willingness to buy.

For one, look at interest rates. While car loans are often done with five-year loans, RVs tend to be more expensive and typically fall to the 10-15 year range for financing. Knowing this, looking at the 10-year treasury can give you a simple but effective glance into the fact that interest on these RV loans has become considerably more expensive.

While loans in 2020 could be financed at under 1% interest and below 1.5% for most of 2021, people have to cough up interest around 2% if they were to go and finance an RV today. Compared to the start of last year, a monthly payment on a 10-year $100,000 loan has gone up from $876 to $920. That’s a real difference that can hold people back from making a purchase, especially when considering the retail cost of an RV has surged upwards of 30% in many cases according to executives in the latest Winnebago conference call.

The other major cyclical drag on demand is the cost of ownership. A major driver in this is rising gasoline costs, which are currently at their highest price nationally since September of 2014. Keep in mind the current national average of about $3.46 per gallon does not include most of the over 20% surge in oil prices that have occurred so far this year.

If you assume this surge will bring national gas prices back to their pre-2014 crash levels of around $3.75 per gallon. Compared to the national average at the end of 2020 of just $2.33 per gallon, you’re paying almost $150 more per tank on a Class A RV that holds 100 gallons, or about $35 more per tank on a Class B or C that holds 25 gallons.

Adding on the fact that monthly insurance premiums have been going up, you’re looking at your cost of ownership being hundreds, if not thousands of dollars per year more expensive than they were just 12 months ago depending on the lifestyle of the buyer.

Putting these factors together, consumer price elasticity can certainly drag demand at these levels. I normally don’t glean too much into sell-side analyst expectations, (my Facebook piece from early January and my Build-A-Bear coverage show why), but the expectation that negative year-over-year comps could emerge in the RV space as 2022 progresses is not something that I disagree with.

The market certainly doesn’t disagree either, with its valuation of stocks in the RV space exemplifying the concerns about upcoming headwinds. The valuations also emphasize the concern of potentially shrinking margins. Some of the margin gains seen in the space have been anticipatory pricing ahead of inflation, but pricing can only go so far with growing consumer frustration over retail prices. On top of this, the expectation that the supply/demand imbalance in the RV space could resolve this year would create a scenario where discounting may become more prevalent in the space again, something that could press margins further.

With these problems becoming an issue, it begs the question of how companies in the industry plan to fight back against these cyclical headwinds. Winnebago has made their answer abundantly clear: acquire secular tailwinds.

The Boon of Pontoons

For years Winnebago has pursued a strategy of inorganic growth. Through selective acquisitions, the company has been able to grow its market share in RVs from just 3.3% in 2016 to 13.3% by October of last year. Starting with Grand Design in 2016, the company has used cash and stock to finance its buyouts. And unlike Tenneco which I wrote about last week, Winnebago has been able to reduce its leverage as promised after acquisitions. The company is even under its target leverage ratio of 0.9x-1.5x as I’m writing this, so maybe there’s the potential for another acquisition out there, but saying anything with confidence regarding that would be unfounded.

In what I see as an acknowledgment that headwinds would be approaching the industry, Winnebago announced in July that they were making their first acquisition of a company in the boating industry with an annual sales run-rate of over $50 million, Barletta. Importantly, these end customers tend to be wealthier than the average RV customer, reducing the impact of consumer price elasticity that has begun to show up in the RV space. The acquisition is also accretive to margins, pushing back against the emerging RV pressures.

Buying the company for an initial consideration of $255 million, Winnebago is entering a segment that faces far fewer headwinds in pontoon boats. For a variety of reasons such as the larger deck space allowing for more people, the family-friendly and recreational tilt, and better stability on the water among others that are highlighted in articles like this one, pontoon boats have become increasingly favored by buyers.

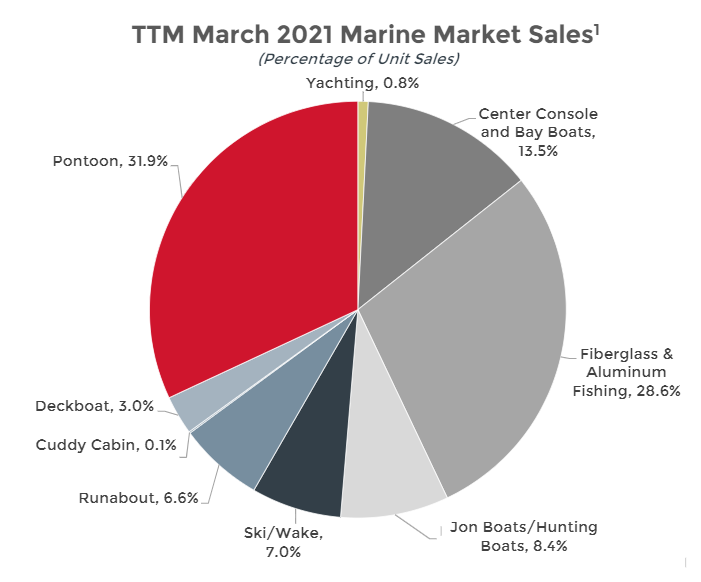

This popularity has propelled meaningful market share capture for pontoon boats. From seeing year-over-year share gains in this 2017 report to recent data showing growth to almost a third of the boating market the continuation of this trend serves as a material tailwind for the space.

A notable point in the acquisition is that Barletta is quickly gaining market share in the pontoon market, something that orients itself strongly with Winnebago’s objectives in the RV market of growing market share. Since being founded in 2017, Barletta has already captured 5.3% of the pontoon boat market and saw major unit growth in 2020 and early 2021 compared to peers that were struggling to expand their growth rates. The latter point is particularly important considering there have been meaningful supply chain issues in boat production. Even in late 2021, these only cut units sold for Barletta by around 5% when the pontoon market as a whole saw 30%+ declines in sold units. Superiority in supply chain management has allowed them to further enlarge their market share

That fact shouldn’t be a surprise considering Barletta was founded by Bill Fenech, the same person that was also a founder of Grand Design. That company has been a major driver of market share gains for Winnebago as a whole, and his role in Barletta makes it seem believable that Winnebago’s acquisition could allow it to become a major player in the pontoon boat market. I don’t doubt that double-digit market share in the space is a possibility as Grand Design has contributed to similar numbers for the RV segment of the company.

Another boon to the boat market can be found within the channel checks that I discussed earlier. Pre-bookings remain strong, indicating that there has been less demand pulled forward in pontoon boats by the pandemic when compared to RVs. Importantly, this has led to a larger supply/demand imbalance in the boating industry that will take longer to normalize. This was highlighted in Winnebago’s latest conference call.

And the last category I would point out that we believe will take the longest is the boat category. Pontoons and the luxury runabouts (Winnebago Q1 conference call)

The combination of these cyclical supply/demand imbalances and secular growth opportunities in the pontoon boat space give Barletta the ability to continue growing, while their business strategy and more efficient supply chain management allow them to gain further market share.

While I would anticipate deceleration from the 60% revenue CAGR Barletta has had since its founding, I would expect substantial growth as they scale with Winnebago. There’s a reason that the marine segment of Winnebago is expected to quickly grow in revenue and profit share after all.

The Bottom Line

Typically, as a company acquires more business, each additional acquisition adds incrementally less shareholder value per dollar than the prior one. But I don’t see that being the case with Winnebago. Their ability to adhere to leverage commitments, gain market share and aim to limit the impacts of cyclicality on their business give an interesting use case into how selective acquisitions and inorganic growth can work when done right.

While a shareholder wouldn’t necessarily be pleased with the dilution caused by their strategy, (the stock would be at $82.5 today instead of $65 if they didn’t use stock to fund acquisitions and this dilution mostly occurred at prices in the $20-$40 range), you can’t deny the positive impact they’ve had for shareholders.

A company whose stock had negative returns for 13 years from 2003 to 2016 has almost tripled since announcing its first major acquisition as a part of this capital allocation strategy. That’s something worth paying attention to, and I’m interested to see how their entrance into the pontoon boat market works to hedge against the cyclical headwinds facing the RV business.

I wanted to end this week’s note by thanking everyone for your support in the past week. We’ve seen the subscriber count of this newsletter double to almost 175, largely due to recognition around the Facebook bear thesis I posted a month ago. I’m incredibly thankful that people think my writing is worth their time and have appreciated all the feedback I’ve gotten to date.

As I want to keep making this project bigger in the future, I also want to put it out there not to expect perfection from me. As someone gets a bigger audience and scales, people expect bigger results and more accuracy. While I will do my best to improve quality every week, every content creator puts their heart into improving, there is a hard limit to how accurate you can get in the stock-picking universe. Even the best stock-pickers are wrong almost half the time.

There’s cognitive dissonance in growing an audience and scaling a publication while also having to admit you will be constantly wrong in the future. That’s just the reality of being a stock-picker though. I’ve had great conversations with mentors and professors in the past week, and there was one constant theme in their advice about being a professional in the markets. Stay humble.

Thank you again, it means the world to me.

- Strat

Follow me on Twitter and Commonstock

Watch my Twitch! Streams will be every Monday at 6:30pm ET!

Join my discord server! https://discord.gg/M4sc9EexBa

View my notes for this week’s piece here

https://cdn.discordapp.com/attachments/764703716217323540/940437785511358515/vocodes_2bf320a3-2d75-4cc6-906b-d7c15001cff4.wav