Hycroft Mining's Retail Trader Scam

How Hycroft Mining is ripping off individual investors to the tune of millions

Hycroft Mining (NASDAQ: HYMC - $83 million) is a company that is engaged in the exploration, mining, and development of the Hycroft Mine in Nevada. They also have a history of failure including bankruptcy, a SPAC merger where the CEO and CFO resigned within two months, a complaint with the SEC that they did not honor obligations to warrant-holders, a required royalty payment to a major shareholder and creditor, and have discontinued mining operations due to the inability to control costs, meet gold recovery rates, and properly deploy leach pads.

To top it all off, their “saving grace” investment from AMC Entertainment (NYSE: AMC - $8.28 billion) seems to be a ploy between a major investor and creditor of Hycroft and AMC to provide a retailer-trader induced liquidity frenzy to sell massive amounts of stock rather than something that has real prospects of leading to operational success. What’s more, “AMC influencers” may have been trading Hycroft before the announcement with insider information.

Hycroft Mine: 40 Years of Failure

While Hycroft Mining was near the brink of bankruptcy just two weeks ago, the Hycroft Mine itself has a much longer history than the company it’s named after. Not surprisingly, its history is about as checkered as they come despite their claims of having one of the largest gold deposits in the world.

The mine itself first had operations on it begin in 1983, almost 40 years ago. A few years later in 1987, the mine was bought by Vista Gold Corp. Despite efforts, the mine could not succeed, and operations ceased in 1998 and didn’t resume until after Hycroft Mining’s predecessor, Allied Nevada Gold, bought the mine in 2007. Again, the mine was a failure and Allied Nevada went bankrupt in 2015 with over $500 million in debt, halting operations.

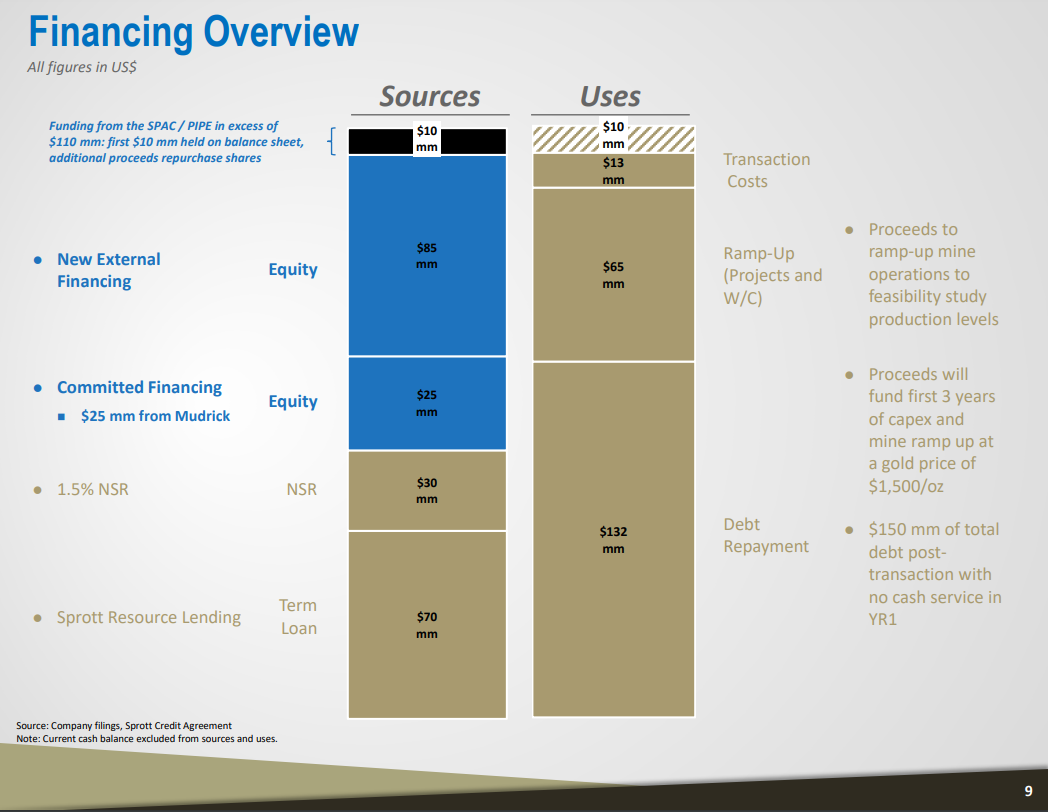

The reorganization of Allied Nevada Gold is what led to the birth of Hycroft Mining in 2017. Mining operations restarted in 2019 but were generating large losses that were leading to liquidity strains on the business. Needing to tap liquidity, Mudrick Capital Management, a major investor and creditor of Hycroft Mining, used one of its SPACs to buy Hycroft, injecting $85 million of public investors’ money into the business in a dubious manner.

Even with the SPAC money, more financing was needed, which led to one of the wackiest and most obscene agreements I’ve ever seen made by a public company. Sprott Resource Lending, headed by Eric Sprott, one of the people who gave money to Hycroft with AMC last week, also gave the company money as part of the SPAC deal. But strings were attached, including a required royalty imposed on the business.

On May 29, 2020, the closing date of the Recapitalization Transaction, the Company and Sprott Private Resource Lending II (Co) Inc. (the “Payee”) entered into a royalty agreement with respect to the Hycroft Mine (the “Sprott Royalty Agreement”) in which Payee paid to the Company cash consideration in the amount of $30.0 million, for which the Company granted to Payee a perpetual royalty equal to 1.5% of the net smelter returns from its Hycroft Mine, payable monthly. (Hycroft Mining Q2 2020 Form 10-Q)

Not only did Hycroft agree to give Sprott 1.5% of net smelter returns from the mine, but this was agreed to in perpetuity. In my opinion, this speaks volumes about the pressure the company was under financially and should’ve been a red flag to any potential investors in the company as it went public.

What should’ve been just as alarming was the collapse of the management team. Under two months after the SPAC merger was announced the CEO of Hycroft Mining, Randy Buffington, resigned from the company. Less than two months later the interim CEO who was initially the CFO, Stephen Miller, also resigned from the company the moment a replacement CEO was found.

While one can speculate about the actual reasons behind their sudden departures, disgruntled shareholders claim that it was to get out of the spotlight before unwelcome news could surface. On September 21st, 432 investors filed a complaint with the SEC against Hycroft and Stephen Jones alleging that the company had acted in bad faith when it issued warrants, publishing a 29-chapter book detailing their complaint.

In total, over $600 million is alleged to have been stolen from warrant-holders by Hycroft as a result of the company not honoring the obligations they were tied to. I’m not in a position to state the accuracy of the claims made in the complaint, but the precedence from the company has dark comparisons to what is currently happening to retail investors that I will touch on later.

While this was ongoing, the financial condition of the company remained in a crisis. On August 10th of 2020, under three months after entering the public markets, Hycroft Mining issued a going concern stating that it may be unable to meet its financial obligations within the next year.

Although the Company recently completed the Recapitalization Transaction with MUDS, using its internal forecasts and cash flow projection models, it currently projects there will be insufficient cash to meet its future obligations as they become due as the Company continues to ramp up the Hycroft Mine's operations from current levels or to levels which are contemplated by the 2019 Hycroft Technical Report. (Hycroft Mining Q2 2020 Form 10-Q)

The going concern also stated that the company had been unsuccessful in achieving its operating cost targets due to a myriad of reasons that had caused further strain on the business. At the same time, it was revealed that the company had to write off over 6,500 ounces of gold from its inventories due to improper processing, costing the company an additional $10 million.

By the end of September 2020, Hycroft’s cash balance had fallen to just $11.5 million, down over 75% from three months prior. Needing to stave off solvency issues, the company issued a secondary offering at a 25% discount to prices it was trading at just two weeks prior, diluting existing shareholders.

Despite these issues, the company’s third-quarter form 10-Q stated that they forecasted operating cash flow to be break-even or green by the end of the second quarter of 2021. It was hoped that the new money would bolster the business, but these hopes were dashed in March of last year when the company reported its full-year results.

A “shift in focus” had led to a 90-day delay in the leach pad expansion project becoming indefinite as test pads had to be sent back to labs for further testing, mining output being called to decrease by two-thirds after April ended, and the going concern stating that operations may have to be limited. At this point, the stock was down over 60% since its SPAC merger that had occurred under a year prior.

This “shift in focus” did not lead to better results for Hycroft. on November 10th, the chairman of the board, David Kirsch, resigned and the company discontinued mining operations. The decision was blamed on higher operating costs across the board, an inability to replicate a high correlation between oxidation rates and gold recovery, and other factors. Despite the recent news, mining operations have not resumed to my knowledge.

An unfortunate impact from the shuttering of mining operations was more than half of the company’s 209 employees being laid off. Knowing that despite the firings the CEO and CFO have kept their base salaries of $550,000 and $375,000 respectively through this decline, worth 34% of the current year’s estimated sales by the only sell-side analyst, is unconscionable to me. Combined with all insiders owning just 1.33% of the company on March 1st, or just $250,000 shows a lack of alignment with shareholder interests that will become important as we move to the next part of this piece.

The Scam of Retail Traders

By early March Hycroft was in a precarious state. With their primary driver of revenue not in operation and their cash balance dwindling to just $8 million according to a source, the company needed immediate cash to not face bankruptcy for the second time in under a decade.

Hycroft had filed for a mixed offering of up to $500 million, but there was a problem. To raise money from a secondary offering, you need liquidity in the underlying security. At this point though, Hycroft’s stock was only seeing a notional value of under $100,000 traded per day, oftentimes under $50,000 per day. With such a lack of liquidity, the company could not raise funds through the equity market.

This is where the founder of Mudrick Capital, Jason Mudrick made a move that I can only describe as dubious. Remember, Mudrick had already used its own SPAC to inject Hycroft with capital, so this isn’t the first-time questionable methods have been used to raise capital for the company.

Jason Mudrick, the firm's founder and chief investment officer, called Aron last week asking him to advise Hycroft on how it could launch a stock market offering to stave off bankruptcy, the person familiar with the matter said… Mudrick knew Aron because he had previously invested in AMC and participated in a debt restructuring deal in 2020 that helped keep the movie theater operator afloat. (Reuters)

The Reuters article essentially claims that Mudrick leveraged his role in helping bail AMC out in 2020 to help secure a cash investment into the business. That’s business, but why would a movie theater company be anywhere near an ideal investment partner for a gold company? In my mind the answer is simple. Liquidity. And saying this is not an outlandish claim, Adam Aron outs that as a reason in his tweet announcing the deal.

How does a movie company give liquidity? It’s not primarily through the $22 million in cash that they gave Hycroft Mining, but the trading volume on the stock that their investment would bring. Everyone knows there’s a cult following of retail traders on AMC’s stock despite the horrendous fundamentals.

Even now you can run into Twitter spaces near daily with hundreds of people talking about why “MOASS has to happen,” and they will follow what Adam Aron and AMC do without a second thought. This is a fact that Hycroft Mining exploited to likely sell massive amounts of stock during the trading frenzy that ensued on March 15th.

Within minutes of AMC’s investment into the company being announced Hycroft filed an 8-K form announcing their agreement with B. Riley to conduct a secondary offering of up to $500 million of stock. With the massive volume surge of over 330 million shares traded on the day of the announcement alone, I don’t doubt that a large number of shares were sold into the market, though I cannot confirm this until the company files information related to this at a future date. Note this also means the current market cap is likely outdated and is probably well higher along with the share count.

To put in perspective the dilution that would occur if $500 million of stock was sold, the diluted shares outstanding would quadruple if they sold only at the highest price observed since the offering was announced. If the average selling price were at Friday’s closing price of $1.35 per share, the diluted shares outstanding would increase more than seven times over.

On top of the moral issues of convincing retailer traders to swarm to a near-bankrupt mining stock that currently has its mine closed to majorly dilute them in the process, it’s possible that “AMC influencers” who use their large platforms to convince people to buy and hold AMC stock, may have been trading Hycroft Mining’s stock before the investment was announced using material non-public information.

Take this example from TaraBull, one of the largest “AMC influencers” with over 75,000 Twitter followers. She publicly admitted to buying Hycroft’s stock before the announcement of AMC’s investment was made.

When I commented on the suspect nature of this, she replied by saying she bought the stock because of the “Nickel squeeze.” Though I can’t confirm that illegal trading was done, buying a gold and silver company with a closed mine to take advantage of a short squeeze in a completely different commodity makes no sense in my mind.

Questionable trading activities don’t end with this person though. Call option volume expiring the week of the deal exploded leading up to the announcement.

Closing Thoughts

While the actions of the last week may have prevented bankruptcy for Hycroft Mining, that does not mean the company’s future is bright. The Hycroft Mine has been a cash drain for almost half a century, and the company may still have not raised enough capital to put its operations into motion in a sustainable manner.

Furthermore, the ethics behind what has been done to retail traders are highly questionable at best to malicious at worst. It appears that individual investors that trust the word of people like Adam Aron were funneled into a near-bankrupt company to give the stock liquidity to dilute the individual investors. I don’t think I’ve seen actions taken to deliberately harm shareholders in such a way before.

I would try to model out financials to understand a potential fair value of the company, but not knowing the amount of dilution that has occurred in the past week makes this task impossible. Despite this, the red flags in both the long history of the mine itself and Hycroft Mining since its SPAC merger lead my opinion to be that the stock may resume its underperformance in short order.

This article is not investment advice and only represents the thoughts of Strat Becker. You can reach me by email at RealStratBeckerYT@gmail.com, on Twitter @StratBecker, or on Commonstock @Strat. This article is for subscribers of the Theta Thoughts newsletter. If this was shared with you please consider subscribing to receive free stock analysis like this every Monday.

Disclaimer: I hold no position in Hycroft Mining and am receiving no compensation to write this article.