Tenneco's Leverage Dilemma

What was supposed to be a quick acquisition and spinoff has turned into a massive slog. But can it be turned around?

New analysis is posted every Monday at 10 am ET. Subscribe to Theta Thoughts to get posts that give you a premium for your time directly in your inbox!

Disclaimer: I hold no position in Tenneco. This and all posts on Theta Thoughts are my thoughts alone and should not be constituted as investment advice

We’re back at college! Well as back as driving three hours to take night classes two days in a row before a snowstorm is. At least I made it here before the blizzard!

Since this week’s piece is on leverage, I wanted to bring up a crazy point about leverage in trading that can also explain why retail investors are facing such steep declines lately.

Half of retail options are leveraged yolos? Now things make more sense. With that out of the way, onto the show!

Some context before we get to the details. Tenneco is one of the larger auto part suppliers today. Despite a market cap of around $1 billion, the company does over $17 billion in sales annually. This is caused in part by the company’s history. Prior to 2018, Tenneco had two segments: Clean Air (CA), and Ride Performance (RP). Despite having over $9 billion in organic sales, the company was never the largest peer in its markets and was seeking a way to scale in ways that it could not on its own. That’s when it met Federal-Mogul.

A Major Acquisition at the Wrong Time

It’s early 2018. Tenneco was growing for several years since the Great Recession, but began facing potential long-term issues as its smaller portfolio of items is overly reliant on powertrain items, the company was not well-positioned for the shift from “goods” to “services” as replaceable parts are declining, and was competitively weak in the fully-electric vehicle market. The company’s profit margins were beginning to face pressures after 2016, and broader changes were needed to maintain shareholder value in the future.

Struggling to find organic methods to address their issues, Tenneco looked outward to acquire a solution. They thought they found the answer to their dilemma in Federal-Mogul, making a massive buyout in April of 2018. The CEO was optimistic, saying…

Federal-Mogul brings strong brands, products and capabilities that are complementary to Tenneco’s portfolio and in line with our successful growth strategies. (Brian Kesseler in April of 2018)

This $5.4 billion deal was not supposed to be a traditional acquisition though. Rather than just integrating Federal-Mogul and their expanse of product lines alongside other synergies, management had a different vision. They would synergize complementary parts of the two companies, then split the company into two separate entities. The Aftermarket & Ride Performance businesses would be spun off as “DRiV”, and the Powertrain components would remain with the original company. The result of this was proposed as a powerful sum of parts thesis that would generate large shareholder value.

This vision of this plan seemed to be something that the majority shareholder in Federal-Mogul, Carl Icahn, believed staunchly. rather than just taking cash in the acquisition, he also acquired over 9 million shares of the combined company’s class A stock, though this position has been cut in almost half since.

The reality is that the acquisition could not have come at a worse time. At the time of the acquisition annualized light-vehicle production in the United States had begun to decline. Simultaneously, a broader recession in manufacturing started in late 2018 that was still ongoing as the Covid market panic in early 2020 began.

The result of the declining economic conditions was that the combined company failed to reach their pre-stated profit and EBITDA expectations by a wide margin. Aiming to have a combined annual EBITDA of over $1.6 billion or a quarterly average of over $400 million, the company failed to reach even 75% of its objective prior to the onset of the pandemic.

The Leverage Conundrum

The failure of the combined company to reach their profit objectives quickly became a problem. Not only was the spin-off of DRiV partially reliant on proper synergies ahead of time, but it also created a crisis with the amount of leverage the company had on the books.

When buying Federal-Mogul, Tenneco did not have enough cash on hand to fund the acquisition without tapping equity or credit markets. Not wanting to dilute shares of the combined company further, they chose to tap the credit markets, taking out over $3 billion in term loans alongside other debt to finance the purchase. In total, the company increased its long-term debt from just $1.3 billion to over $5.6 billion to buy Federal-Mogul.

To put it in perspective, the tangible book value of the company went from being over $650 million in the positive to being over $825 million in the negative because of the transaction and added debt. This meant that for the combined company to be sustainable, it had to quickly produce cash flow to deleverage itself, something it was explicitly failing to do at necessary levels.

The inability to deleverage meant that the spin-off, which was originally proposed to take place in mid-2019, was postponed to mid-2020 in short order. The pandemic worsened this problem, causing an indefinite postponement of the spin-off in 2020, with discussion of it still not on the table to date. Even today, net leverage has not fallen below 2.9x, and increased to 3.2x in the third quarter of 2021 as annualized vehicle production rates in the US have plummeted due to the semiconductor shortage.

The persistence of this issue is only exacerbating the leverage issues for the company. Annualized light vehicle sales have fallen from over 13 million in October to just 12.43 million in December, almost back to the lows of September. The longer the chip shortage persists, the more prolonged a process of deleveraging will become.

The Path Forward

Despite Tenneco’s failure to deleverage to date, their ability to remain profitable in a constrained production environment and generate high amounts of cash flow relative to their market cap is a positive indicator that the company can successfully begin to deleverage in a normalizing environment. To this point, sell-side analysts anticipate that the company will be able to reduce its net debt position by about $2 billion by the end of 2025.

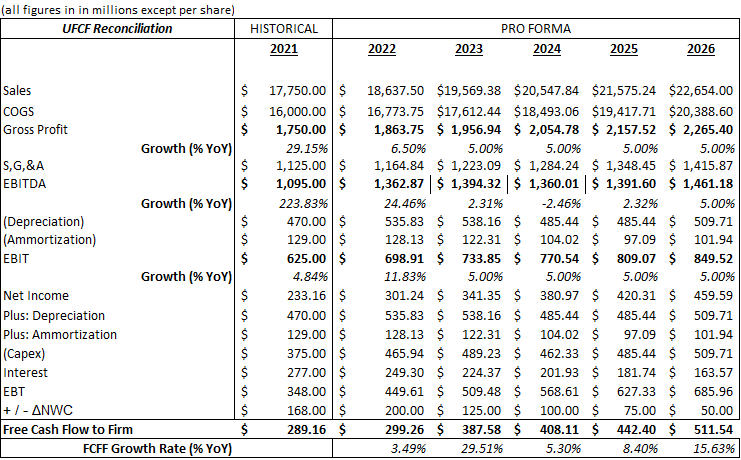

I wanted to see a range of options on how forward growth and leverage levels would impact potential implied stock prices to see if what the sell-side is expecting made sense. To do this I made a discounted cash flow model which you can see below.

The following were the assumptions in this model:

Revenue growth from 2022 onwards is flatlined at 5% annually

Gross margin from 2022 onwards is flatlined at 10%

SG&A as a % of sales from 2022 onwards is flatlined at 6.25%

Capex rises to 2.5% of sales in 2022 and 2023 before falling to 2.25% of sales from 2024-2026

Depreciation as a % of Capex is 115% in 2022 and declines by five percentage points annually until reaching 100%

Amortization as a % of Capex is 27.5% in 2022 and declines by two-and-a-half percentage points annually until reaching 20%

Interest paid declines by 10% annually. Assumes company-wide interest rate on its debt remains constant at around 5.35%-5.4% and reflects a flatlined 10% annual reduction in total debt.

The model is basic in its assumptions since I have not analyzed the business’s growth prospects in-depth and am focusing specifically on the leverage component. However, I do feel that a 5% annualized growth rate in sales is acceptable with the chip shortage likely ebbing as 2022 progresses alongside this rate being within the company’s long-term average post-financial crisis.

The model is also simplistic on the debt side. I’m keeping the interest rate on their debt flat because there will almost certainly be debt refinancing in the coming years. Its term loans worth over $3 billion mature in early 2023 and 2025, and the company will likely refinance its terms favorably as its financial health and creditworthiness improve. However, rising interest rates in the economy going forward and the timeframe that I’m forecasting limit my confidence in changing the interest rate on Tenneco’s debt.

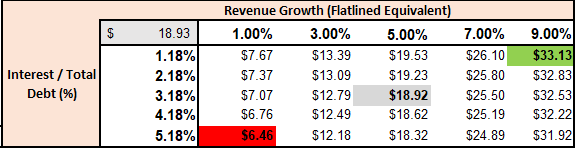

What I can say is that I’m probably being conservative on the debt reduction as time goes on for the conglomerate. By forecasting an annual decrease in debt of 10%, I’m saying that the amount Tenneco’s debt goes down every year will decrease. This is mostly me just being conservative on purpose and puts the $2 billion of net debt reduction over a year behind sell-side’s timetable. With all these factors, I got the following sensitivity table for implied stock prices

As you can see, there’s plenty of upside from today’s price assuming a normalized long-term growth rate can materialize. base case price of $18.92 does use a 3.75x EV/EBITDA multiple but isn’t too different from the two sell-side reports that I also saw models in. Their targets were $17 and $18. What becomes apparent is the importance of the longer-term growth rate. Despite my focus on debt levels in this model, changes in total debt don’t have much impact on the model’s base case because the change in interest payment levels means much less to the resulting free cash flows than the change in revenue. However, it is notable that in scenarios with lower or negative revenue growth, the importance of Tenneco’s debt and leverage increases dramatically in the context of this model.

Takeaways

There are flaws in the model. It would’ve been useful to analyze forward projections with variations on the company’s cost of debt and margins. It also faces the problem that it cannot forecast the impact of an eventual DRiV spin-off, which could occur before 2026 and likely faster if there is better growth and faster debt reduction.

Despite those flaws, I still think the model paints a clear picture. The leverage the company has means there is the potential to drive strong returns if the company can execute and grow strongly, especially if it can be valued as a sum-of-parts in the future rather than as a conglomerate. The downside is also clear. Failure to grow will increase the impact leverage has on the company, and likely make its cost of debt less favorable.

To be clear, just because I ran a model that says a base case of near $19 does not indicate any belief from me that the fair value of the stock is $19. I haven’t gone deep enough into the company to make any determination. I’d also hope the range of outcomes on the model I showed, ($6.46 or a 35% decline to $33.13 or a 200% upside), shows the volatility and uncertainty at play.

I don’t view the company itself as a very good one. It still hasn’t made enough changes to modernize its product line for the shift to electric vehicles. Their original projections in 2018 assumed only 13% of cars would be battery-electric, something that will likely be off by a large margin.

I’m also not a fan of the acquisition of Federal-Mogul. Their first slide in the presentation announcing it preached about how it would generate shareholder value. I don’t think anyone that owned the stock around four years ago is happy with the over 80% decline in the stock price since.

That’s not to say a bad company can’t be a good stock though. Just like I wrote a few weeks ago about Corsair being a good company but not necessarily a good stock, only time will tell what the reality is for Tenneco.

Join my discord server! https://discord.gg/M4sc9EexBa

Follow me on Twitter and Commonstock

Watch my Twitch! Streams will be every Monday at 6:30pm ET!

View my notes for this week’s piece here

P.S. Jimmy Garrapolo is overrated